Should Nixon Have Ended the Gold Standard?

On August 15th, 1971, President Nixon announced before the nation…

I have directed Secretary Connally to suspend temporarily the convertibility of the dollar into gold or other reserve assets.

It’s easy to attack Nixon for ending the gold standard considering what’s happened to the middle class since…

But what choice did he really have?

He originally wanted to wait until after Election Day 1972 to take such a large political risk or as George Schultz would later describe as, “the biggest step in economic policy since the end of World War II” because as Nixon complained to his advisors ending the convertibility of the dollar had little political upside as it’d go over the head of the average voter while having a large potential downside since no one could be sure how far the dollar would fall.

But all his top advisors told him that if he didn’t close the international gold window ASAP then there’d likely be a run on the dollar.

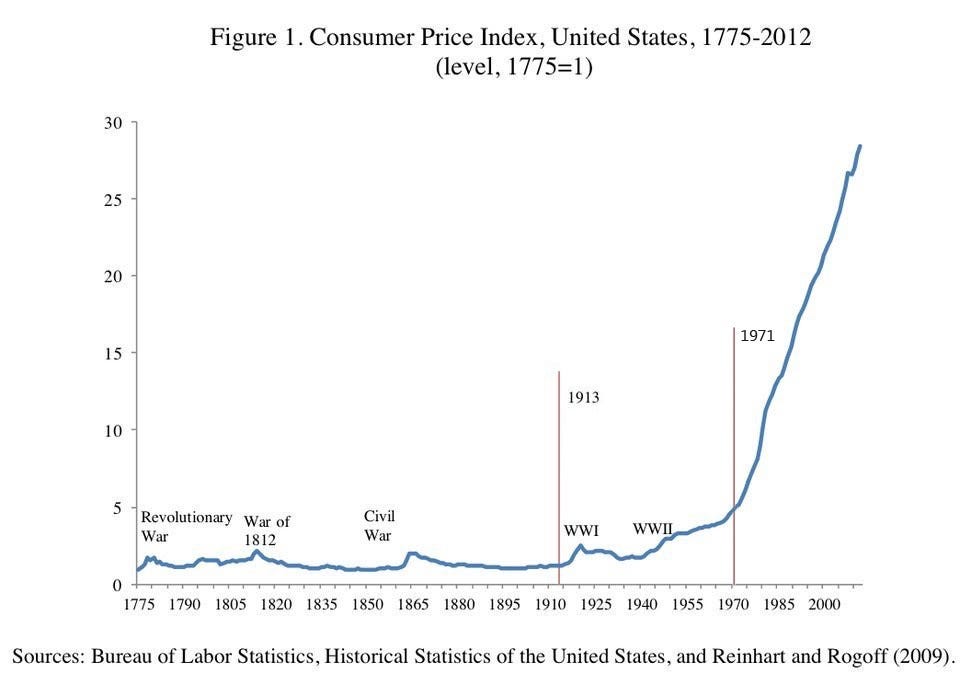

In 1955, American gold exceeded official dollars abroad by over 160%, but by the summer of 1971 it was down to 25%. With reports coming in that the UK was looking to convert some of their dollars into gold, Richard Nixon boarded Marine One and with some of his top economic advisors flew to Camp David for the weekend in order to reach a decision.

Theoretically, Nixon had four options…

He could do nothing, but Richard Nixon wasn’t about to risk his reelection on the hope that foreign politicians and “international money-lenders” wouldn’t run on the dollar before then.

He could reduce the dollar supply by cutting spending and raising taxes, therefore, worsening an already stagnating economy that was experiencing 6.1% unemployment and 5.9% price inflation, but the Democratic House and Senate would’ve never voted for austerity.

He could just devalue the dollar relative to gold. This was after all what a congressional report had recommended just 10 days prior, but this was quickly ruled out by his advisors because it probably would’ve just precipitated a run as countries would suspect more devaluations to come.

Or he could temporarily end it.

In the end, it really wasn’t a choice as all his advisors — Republican, Democrat, and independent — supported “suspension.”

They actually spent much more time at Camp David discussing the pros and cons of price controls and tariffs as well as the all-important issue to Nixon: how to sell his program to the American people.

We’d like to think our elected leaders are cautiously weighing the long-term impact of their policy positions, but Richard Nixon was a great politician because of how little it factored into his discussions. His focus was on winning reelection and so much of the talk at Camp David wasn’t, for example, on how price controls, which Nixon was philosophically opposed to, would at best temporarily suppress inflation, but whether voters would like it and how it could suppress inflation just long enough to get him past Election Day.

Ultimately, the reason the gold standard ended wasn’t that it limited government spending too much, but that it really didn’t limit it at all because as soon as the gold standard looked like it might limit government spending the government would have no choice but to devalue it — unless you consider economic collapse a choice, which if you do doesn’t negate the fact that no democratically elected president would.

Traditionally, when the tide would rise a politician would just build a new sand castle further back, but Nixon refused to because at that point it was clear to virtually everyone that the shtick was up. The gold standard was made of sand.

Virtually every economist is wrong about monetary policy because they’re too focused on monetary rules — gold-backed vs. reserve targeting vs. inflation targeting vs. NGDP targeting — while ignoring the far more fundamental question: freedom vs. monopoly.

Under a monetary monopoly, it doesn’t matter what “perfect” monetary rule you put in place because as soon as the going gets tough it will inevitably break down so long as the only consequence for eroding people’s wealth is that the government will be given even more control over it. The more the bureaucrats fail the more they can blame capitalism.

And then only as a secondary consideration should we consider what monetary rule should constrain the dollar supply.

And so with that said, Nixon’s failure isn’t that he scratched away the gilded floor, but that he didn’t even try to build a stronger foundation via monetary freedom and a more constrained dollar.

A major theme of his speech was after all about making America more competitive again — he said “gold” 1X and “compete” 15X — and so logically he could’ve argued that we should make our monetary system less a socialist monopoly and more of a competitive marketplace with multiple legal tender currencies.

As part of his order to direct Treasury Secretary Connally to suspend the convertibility of the dollar, he could’ve directed him to end the prohibition on the private ownership of gold (as Gerald Ford would do in 1974) and then as part of his New Federalism philosophy he could’ve encouraged the states to make gold and silver legal tender, which the Constitution explicitly gives them the power to do: “No state shall coin money, emit bills of credit, or make any thing but gold and silver coin a tender in payment of debts.”

Another major theme of his speech was attacking “international speculative money lenders.”

He could’ve doubled down on this conspiratorial tone by correctly blaming the Fed for most of our inflation.

He could’ve called for a full audit of the Fed — opponents shoo-shoo it with, “the Fed is already audited” to then contradict themselves by saying how more transparency would “politicize monetary policy” — and over his tenure, he’d appoint five Fed Board Governors so he could’ve appointed individuals who’d increase the Fed Fund rate, but instead he did the exact opposite by appointing Arthur Burns as Fed Chair with the expectation he’d print, print, print in order to forestall a recession until after Election Day.

Of course, none of the measures I put forth here were discussed on that warm summer weekend at Camp David because Nixon was preoccupied with how his hodgepodge of “bold” actions would complement each other to reverse his declining poll numbers, which because he basically stole the Democratic platform to the chagrin of Democratic politicians, he won nearly unanimous approval from its greatest beneficiaries: bankers, bureaucrats, and brokers. To the political strategist, this was triangulation, but to the politically principled this was treachery, and since the politically principled are all too uncommon Richard Nixon went on to win in 1972 with one of the largest landslides in American history. Makes ya wonder — should we really be giving even more power to those who are incentivized to be so manipulative and short-sighted?

To this day both parties have become too sympathetic to the Fed’s monopoly power, but if we had done what I laid out here then we would’ve seen a lot less inflation and debt over the last 50 years and therefore smaller speculative bubbles, greater economic growth, and a stronger middle class.